According to IHS iSuppli's special report on China research, the turbulent global economy is dragging on China's domestic LCD TV market, resulting in extremely weak growth this year.

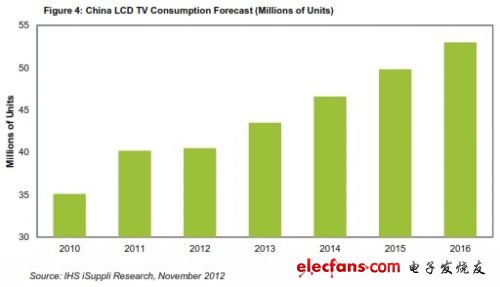

China's domestic LCD TV consumption is expected to reach 40.5 million units this year, only 1% more than the 40.2 million units in 2011. Compared with the year-on-year growth of 15% in 2011, this year's growth is very pathetic. In 2010, the TV consumption in China increased to 35.1 million units.

However, the decline in growth rate will be temporary, and the situation is expected to improve next year. The consumption of the local TV market is expected to increase by 7% next year to reach 43.5 million units. Unless the economy changes unexpectedly, the Chinese market will continue to expand, and domestic LCD TV consumption will reach 53 million units by 2016, as shown in Figure 4.

Figure 4: Forecast of LCD TV consumption in China (in millions)

Despite the good prospects, the sharp growth momentum in 2012 was in sharp contrast to previous years. IHS iSuppli believes that if it were not for the negative impact of global economic uncertainty, the Chinese LCD TV market would have grown strongly.

Three factors will help the market pick up next year: the domestic economy recovers, the Chinese government issues stimulus policies, and LCD TV prices continue to fall.

Chinese manufacturers maintain production momentum

Although the domestic consumption of LCD TVs has declined sharply this year, China's LCD TV output seems to be showing no signs of weakening. In 2012, the output of Chinese LCD TV manufacturers is estimated to reach 75.1 million units, an increase of 8% over 2011.

However, the six largest Chinese LCD TV manufacturers continue to lose money in the TV business. Due to the lack of core technology and the strength of the RMB, it is difficult for major LCD TV manufacturers in China to reduce costs and develop high-end products. Major Chinese LCD TV manufacturers include TCL, Hisense, Skyworth, Changhong, Konka and Haier.

The six largest manufacturers are facing difficulties, but they have brought rare opportunities for second-tier domestic LCD TV manufacturers such as MTC and Tsinghua Tongfang. Due to lower operating costs, the financial status of these second-tier vendors is better than that of first-tier vendors.

Other changes

Other changes are also affecting China's LCD TV supply chain. For example, there are so-called semi-bulk (SKD) and full-bulk (CKD) service providers that produce TV boards with integrated chipsets and are replacing traditional TV manufacturers. Another change is that traditional design companies are declining and their functions are being taken over by semiconductor suppliers. Semiconductor suppliers can now provide TV manufacturers with complete solutions.

In addition, the competition in the field of LCD TV semiconductors in China is fierce, but extremely uneven. Taiwan MediaTek, after annexing Taiwan ’s Morningstar Semiconductor, is a leader in the industry. MediaTek now controls 89% of the Chinese LCD TV chip market. Its rival Realtek only has a 4% share. Realtek is also a Taiwanese manufacturer.

Nine local and foreign companies are fighting for the remaining 7% market. These include Shanghai Jingchen Semiconductor; Taiwan Lingyang Technology, Novatek and SiS Technology; French-Italian company STMicroelectronics entered the market through the acquisition of Genesis; American Sigma Designs entered the market through Trident, in addition to Pixelworks, Marvell and American companies such as Broadcom.

Qualcomm and Nvidia are also considering entering the Chinese LCD TV chip market. TV chips that enter Chinese-made TV sets will increasingly provide complex functional features, including Internet connectivity, 3D capabilities and LED backlight technology.

6-9V Lithium Manganese Battery

Jiangmen Hongli Energy Co.ltd , https://www.honglienergy.com