Before the 1990s, the LED industry was in the early stage of development. The product color system was single and the price was relatively high. The application market was mainly driven by the demand for signal lights, indicator lights, and monochrome displays. The LED industry Entering the stage of rapid development, the development of blue and green light technology and the decline in product prices have enabled LEDs to be rapidly promoted in commercial fields such as small and medium-sized backlights and full-color displays, and became the main driving force for the development of the LED market at that time; With constant maturity and further reduction in prices, LED will gradually penetrate into the fields of home lighting, commercial lighting, industrial lighting, etc., forming a huge potential application market. In the future, with the development of plant lighting, Mini LED&Micro LED, automotive lighting and other industries, LED Will maintain rapid growth.

According to data from the LED Research Institute of Advanced Industry Research (GGII), the overall scale of China’s LED industry in 2017 was 636.8 billion yuan, a year-on-year increase of 21%. The output value of LED upstream chips, midstream packaging, and downstream applications reached 18.8 billion and 87 billion respectively. Yuan and 531 billion yuan, up 29.7%, 18.05%, and 21.79% year-on-year respectively. GGII predicts that the compound growth rate of China’s LED industry output value will reach 18% from 2018 to 2020, and that China’s LED output value will exceed 1 trillion in 2020.

2018 new pattern of led industryAs countries put incandescent lamps on the agenda, the LED that has experienced a round of ups and downs seems to be rejuvenated. Looking at the entire LED industry chain, we can see that the LED chip field is a high-margin link in the LED industry chain. The industry's average gross profit margin is relatively high, and the high profitability will continue in the future:

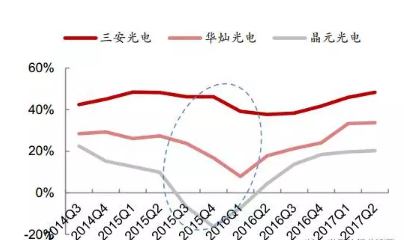

1) After the industry has undergone a reshuffle, low-end production capacity has been eliminated, and large domestic manufacturers have expanded their high-end production capacity on a large scale to seize market share. The industry is moving towards an oligopoly. By the end of 2017, the domestic market share of Sanan and Huacan is expected to increase To 40% and 30%, the capital, technology and scale advantages of large factories will widen the moat.

2) In the upstream MOCVD equipment link, domestic manufacturers such as China Micro Semiconductor and Zhongsheng Optoelectronics have gradually broken the foreign monopoly structure. In 2016, the two domestic market share has exceeded 10%, and localization is expected to promote the reduction of equipment costs.

3) Large chip makers are integrating upstream. San'an and HC Seminar have self-produced substrate sapphire materials, and self-production of raw materials further improves profitability.

Based on this, let’s take a look at the world of LED chips that you don’t know

LED chips are getting hot, and production capacity is shifting to domestic

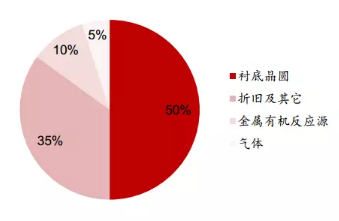

After years of development, the price of LED chips has been reduced through the improvement of light efficiency. The cost of chip production mainly consists of variable costs and fixed costs. Variable costs, including substrates, metal organic reaction sources, and gases, account for about 65%, and fixed costs, including depreciation and others, account for about 35%.

LED chip manufacturing cost

The improvement of manufacturers' technology has brought about the improvement of LED light efficiency. The number of chips that can be cut per unit area of ​​epitaxial wafers has increased, chip costs have fallen, and chip prices have also fallen year by year.

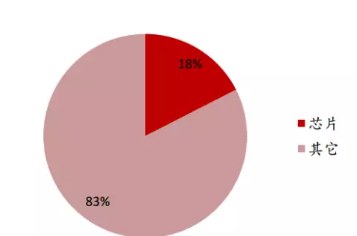

As an important part of LED products, chips account for a high proportion of product costs. Taking general lighting as an example, chips account for 18% of the cost of general lighting products.

Take lighting products as an example, LED chips account for 18% of the cost

The decline in chip prices directly promotes the decline in the price of LED bulbs (the price is about 1.3 times that of energy-saving lamps), and the lower prices promote the rapid increase in the penetration rate of LED lighting. Since 2011, the penetration rate of LED lighting has increased rapidly. By 2016, the global LED lighting penetration rate was close to 30%, and it is expected to exceed 60% by 2020.

The supply-side contraction triggered and drives the LED chip industry to improve. Since 2014, the production capacity of LED chips has been significantly surplus. The prices of LED chips have been continuously lowered and profit margins have been squeezed, which has led to corporate losses. LED chip leader Epistar has reversed its loss by freezing production and increasing prices. At the beginning of 2016, the LED chip leader Epistar took the lead to shut down 20%-25% of the production capacity of blue LED chips. As a leading company, Epistar occupies a large market share, and its supply side shrinks to improve the supply and demand structure of LED chips. In May 2016, Epistar increased the prices of some blue light chips by up to 15%. Afterwards, mainstream LED manufacturers such as San'an and Huacan raised prices, and the industry's oversupply pattern was broken.

LED chip companies have gradually increased prices since 2016

Leading domestic manufacturers such as San'an Optoelectronics and Huacan Optoelectronics benefited from the shortage of high-end LED chip production capacity. In 2017, domestic mainstream chip makers turned to high-end production capacity and expanded production. Sanan Optoelectronics expects to expand production by 30%-40% in 2017. HC Semitek will more than double the expansion due to years of continuous deployment of high-end products and large-scale research and development With investment, the performance of HC Semitek and Sanan Optoelectronics in high-end chips has reached the international leading level.

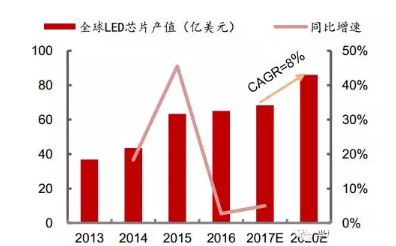

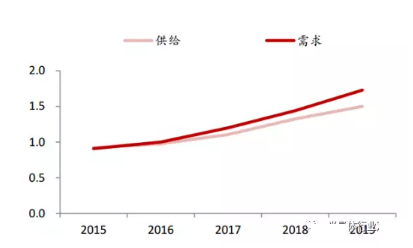

The growth of downstream demand is one of the ways to digest new capacity. The LED lighting industry accounts for the largest proportion of LED applications, accounting for 48% of the overall application market, and its demand will also drive the development of the LED market. The market size of the global LED lighting industry in 2016 was approximately US$35 billion, and it is expected to increase to US$65 billion by 2020, which will stimulate the digestion of new capacity. Affected by demand growth, the compound annual growth rate of LED chip output value from 2017 to 2020 will reach 8%, and by 2020, the global LED chip output value will exceed 8 billion US dollars.

LED chip industry market size (100 million US dollars) and future growth forecast

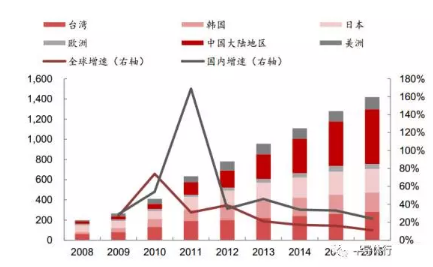

The global market share of China's LED chips continues to increase, and the transfer of overseas orders will be another important way to digest new capacity. After the reshuffle of the LED industry, overseas LED chip companies cut production, Samsung and LG shut down some of their production capacity, Cree cut production on high-power chips by 25%, and foreign chip companies handed over some products to domestic companies for processing. In 2016, domestic chip exports accounted for The total output value of domestic chips was 9.6%, an increase of 1.6 percentage points year-on-year. At the same time, the domestic production capacity growth rate was 24%, which exceeded the global growth rate by 13 percentage points. In 2017, the reduction of foreign epitaxial chip production and the shift of orders to domestic orders will continue.

Overseas companies continue to reduce production of epitaxial chips [Left axis: Regional production capacity (10,000 pieces/month, calculated based on 2 inches), Right axis: Growth rate (%)]

The transfer of overseas orders is mainly due to the fact that overseas LED chip companies are not as competitive as domestic ones, and the growth of domestic LED chip manufacturers is more promising. The relatively stronger profitability of domestic LED chip companies will help scale expansion. Compared with Epistar, HC Semitek and Sanan Optoelectronics have better profit indicators such as gross profit margin and net profit margin. Although Epistar has large operating income, its profitability is poor due to high production costs. Most overseas LED chip factories have similar profit problems with Epistar, and their competitiveness is not as good as that of domestic companies. However, overseas chip production capacity still accounts for a relatively high proportion, so there is still room for continued growth in orders brought about by overseas production capacity transfer.

In the context of overseas production capacity transfer, downstream demand growth, and large domestic manufacturers' vigorous expansion of production, we have roughly estimated the supply and demand of the LED chip industry in the next few years. The calculation of LED chips is adjusted on the basis of epitaxial wafers. The output of epitaxial wafers is calculated based on the number of MOCVD equipment. The calculation is based on the whole year, and it is assumed that the demand for chips in 2016 is 1.

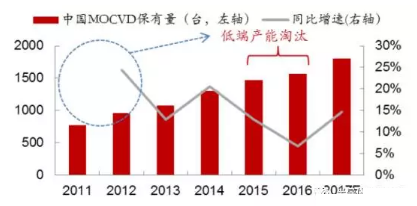

On the supply side: 1) Overseas production capacity is shut down, and domestic production expansion. 2) Low-end production capacity is gradually phased out. Taking Veeco as an example, the equipment faces a major upgrade every 4 years. In the future, the 2012-2014 models should be phased out. About 800 units of K465i-equivalent MOCVD purchased globally are currently maintained globally. The volume is 3100 units, and it is conservatively estimated that 100 units will be eliminated every year.

Demand side: 1) With the evolution of cost, the number of chips that can be cut by a single epitaxial wafer increases. According to an average annual light efficiency increase of about 10%, the number of chips that can be cut increases by 1.1 times. 2) The scale of the downstream application market grows. According to Trendforce's forecast, the compound annual growth rate of the global application market is 8%. Considering that the cost of the chip drops by 10% every year, the epitaxial wafer shipments are converted.

According to calculations, with the clearing of low-end equipment, we expect the current round of supply gap will continue from 2017 to 2019

Global LED chip supply and demand forecast

The competitive landscape of the industry has improved, towards an oligopoly

The industry has undergone a reshuffle, showing a monopolistic competition pattern. Driven by the dual drive of industry development and government subsidies, a large number of manufacturers have poured in, resulting in a relatively fragmented industry competitiveness. In 2015, Epistar provoked a price war to expand its market share. The price of LED chips in the market fell precipitously, and the gross profit margin of chip manufacturers fell.

15Q4-16Q1 Chip manufacturers have low gross profit margin

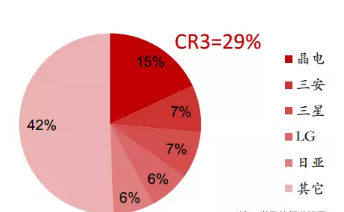

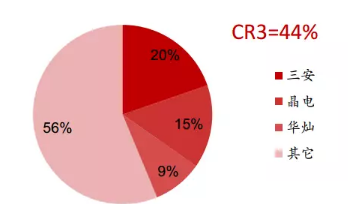

Under the market environment of price diving, small factories with backward equipment and technology have low production efficiency, unsupportable costs, and obvious crowding-out effects. In 2009, there were more than 60 domestic manufacturers, but only about 20 in 2016, and the industry has undergone a reshuffle After that, the degree of concentration increased sharply, with CR3 rising from 29% in 2009 to 44% in 2016.

Global LED chip competition landscape in 2014

The global LED chip reshuffle in 2016 presents an oligopolistic competition pattern

After low-end production capacity was eliminated, the industry's overcapacity situation was reversed, and the global LED epitaxial wafer supply and demand situation improved.

In 2016, the global LED epitaxial wafer supply has been less than the demand (unit: 10,000 wafers)

The improvement of the supply and demand structure has brought about the gradual release of manufacturers' profit margins. In 2016, chip prices have gradually recovered, and chip manufacturers' gross profit margins have been restored.

With the transfer of overseas production capacity to China, large domestic factories have advantages in capital, technology and scale, and actively expand production and seize market share. At the same time, the MOCVD, which was greatly expanded by domestic small manufacturers in 2011-2012, was not as efficient as new equipment, and was eliminated as low-end production capacity in 2015-2016. Taking into account the reduction in government subsidies, small factories do not have the financial capacity to purchase new equipment. Equipment, small factories are shut down, and the reshuffle effect is obvious. The market share of large domestic factories has further increased, competition is more concentrated, and the industry is moving towards an oligopoly. It is estimated that by the end of 2017, the domestic market CR2 will reach 70%, and the market share of domestic giants San'an and Huacan will reach 40% and 30% respectively.

2011-2017 domestic manufacturers' MOCVD equipment holdings

The advantages of large factories have been highlighted, which has increased the barriers to entry in the industry. The capital and technology required by the LED chip industry have high barriers. In terms of capital, the scale of fixed assets of chip manufacturers generally exceeds 1 billion yuan. Taking MOCVD, the necessary production equipment for epitaxial wafers, as an example, the price of 124 chips in 2016 exceeded 2 million US dollars. In terms of technology, the improvement of luminous efficiency requires technical support. The higher the luminous efficiency, the more chips can be cut in a certain area, and the lower the cost. The luminous efficiency of domestic giants such as San'an and Huacan far exceeds the world median. The advantages are outstanding.

Estimated domestic market share by the end of 2017

Domestic equipment cuts in to accelerate the reshuffle of LED chips

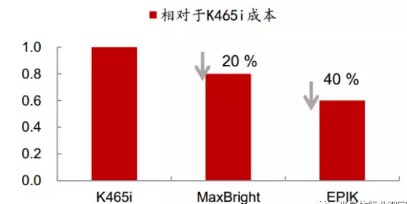

MOCVD is the most important upstream equipment for LED chips. It is mainly used for the growth of LED epitaxial wafers. It has the characteristics of technology as the core, fast replacement and obvious price drop. In addition, due to the continuous investment of leading manufacturers, the equipment factory puts the latest equipment in the leading enterprises in advance, and the commissioning time during mass production is shorter. Technological changes have led to higher efficiency and lower costs: Taking Veeco's third-generation MOCVD equipment as an example, the single-batch capacity of the EPIK series equivalent to 2-inch wafers is 4.4 times that of K465i, while the cost is reduced by 40%.

Taking Veeco as an example, the MOCVD equipment has a short update cycle

Cost comparison of different models

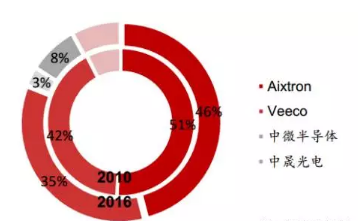

Domestic MOCVD manufacturers have entered the supply chains of San'an and HC Semitek with their price advantages, and the monopoly of foreign manufacturers has gradually been broken. In 2016, the domestic market share of local companies Zhongwei Semiconductor and Zhongsheng Optoelectronics' MOCVD reached 3% and 8%, respectively, and the domestic market share of MOCVD exceeded 10%.

The market share of domestic MOCVD equipment has exceeded 10%

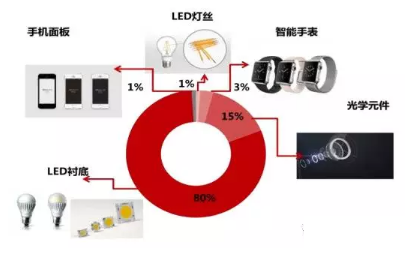

The substrate required for LED chips is the main application of sapphire, accounting for 80% of the application structure in 2016.

In 2016, LED substrates accounted for 80% of sapphire applications

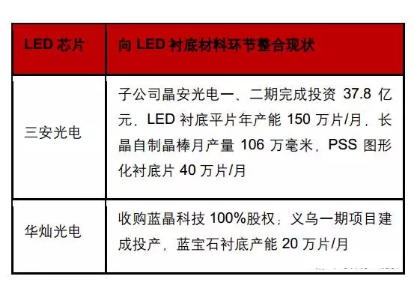

In recent years, LED chip manufacturers have integrated upstream substrate materials. For example, leading manufacturer San’an has deployed sapphire substrate business through its subsidiary Jing’an Optoelectronics. HC Semitek has integrated upstream through the acquisition of 100% of Lanjing Technology. Both giants have Possess self-production capabilities. Through forward integration, the foundation for high profitability will be further laid.

LED chip manufacturers integrate upstream substrate materials and have self-production capabilities

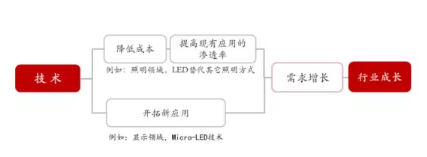

Technology promotes industry growth, Micro LED leads the trend

Technological development will dominate the future direction of the industry, and manufacturers with technological strength will stand out from the competition. On the one hand, technological advancement can reduce costs and increase the penetration rate of LEDs in existing applications such as lighting. On the other hand, technological advancement can open up new applications. For example, Micro LED can be used in the display field, which is expected to promote the demand for LED chips. The increase in volume.

Technology is the core factor for the development of the LED chip industry

Micro-LED (Micro-LED) refers to LED miniaturization and matrix technology. Integrating a high-density and small-sized LED array on a chip makes it about 1% of the current mainstream LED size. Each pixel can be addressed and individually driven to emit light, reducing the pixel dot matrix from millimeters to micrometers.

Micro-LED undertakes the high efficiency, high brightness, high reliability and fast response time of LED, while the power consumption is only 10% of LCD, and the color saturation is close to OLED, which is regarded as the perfect application of new generation display technology. Compared with OLED, which is also a self-luminous display, the brightness of Micro-LED is 30 times higher, and the resolution can reach 1500PPI, which is equivalent to 5 times the 300PPI of the OLED panel used in Apple Watch. The color is also easier to debug than OLED. Longer service life. Because the system's size and weight can be reduced, and it has the characteristics of low power consumption and fast response, wearable devices are the most likely field to be introduced.

With its irreplaceable advantages over LCD and OLED, Micro-LED has broad application opportunities. For display fields with resolutions above 600PPI, Micro-LED is expected to replace LCD and OLED as the mainstream technology for panel displays in the future, and its power-saving characteristics make it suitable for display in wearable devices such as AR/VR helmets and smart watches. It is suitable for outdoor display panels, head-mounted displays (HMD), and automotive head-up displays (HUD). In addition, in the future, Micro-LED is expected to be used in automobile dashboards and consumer electronics, such as notebook computers and smart phones.

In the short term, both large and small sizes are expected to achieve mass production first. From the perspective of industrialization progress, the current industrialization of Micro-LED technology has greater uncertainty, and the smaller the screen, the lower the difficulty of industrialization. For example, OLED was the first to obtain large-scale applications in watches and mobile phones in the field of small screens. As Apple is likely to use Micro-LED display technology in future Apple Watch products, the industrialization process of Micro-LED is also expected to start in the field of small screen displays such as smart watches, virtual reality and wearable devices.

Micro-LED application commercialization mass production speed forecast

The improvement of Micro-LED technology is expected to bring about a substantial increase in chip usage. According to estimates, every 100 million Micro-LED smart watches, computers and TVs will consume more than 700,000, 30 million, and 1.5 billion 2-inch epitaxial wafers. When the annual penetration rate of Micro-LED shipments in consumer electronic terminals reaches 50%, that is, 900 million mobile phones, 20 million smart watches, 220 million computers, and 110 million TVs, which is equivalent to 200 yuan per 2 inch piece. In terms of price, the market size of Micro-LED chips will reach 380 billion yuan, far exceeding the existing 45 billion yuan. There is huge room for market development.

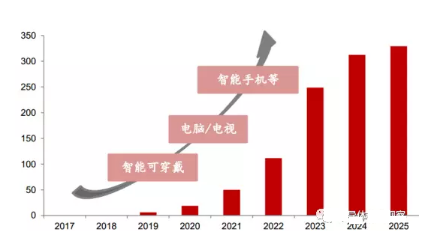

With the gradual breakthrough of technology and cost bottlenecks, the Micro-LED display market is expected to grow rapidly from 2018, reaching a shipment of 330 million units in 2025. According to Yole’s forecast data, once Micro-LED can overcome the existing challenges and establish its supply chain, it is expected to enter the commercial mass production stage from smart watches at the earliest, and accelerate the maturity of its technology and supply chain. Computers, laptops and other fields are gradually expanding applications. The introduction of smart phone applications may take 3-5 years later, but in the future it is hoped that it will quickly penetrate into more than 50% of the display market share.

Micro-LED display market shipment forecast

Machining Parts

Shaft sleeve connector

Shaft sleeve connector

Material: stainless 304

Surface: ultrasonic wave cleaning, passivating

Tube connector

Material: GB20

Surface: trivalent chromium zinc coating

Application: fixed end for control system assembly

Tube guide threaded

Material: stainless 304

Surface: ultrasonic wave cleaning, passivating

Application: control system in Yacht

Control Shaft,Tube Connector,Tube Guide Threaded,Shaft Sleeve Connector

ROYAL RANGE INTERNATIONAL TRADING CO., LTD , https://www.royalrangelgs.com